Tax-Loss Harvesting Offers Chance at Silver Lining

Stock market downturns can be rough on your portfolio’s bottom line, but they may also offer the potential to reduce your tax liability and possibly buy shares at a discount. When an investment loses money, it’s often best to look beyond momentary price swings and hold it for the long term. Sometimes, though, you may want to sell a losing investment, which could help offset gains from selling an investment that has appreciated or reduce your taxable income even if you do not have gains.

Whether this strategy — called tax-loss harvesting — is appropriate for you depends on a variety of factors, including your current portfolio performance, your long-term goals, and your current and future taxable income. Keep in mind that capital gains and losses apply only when investments are sold in a taxable account.

Gains and losses

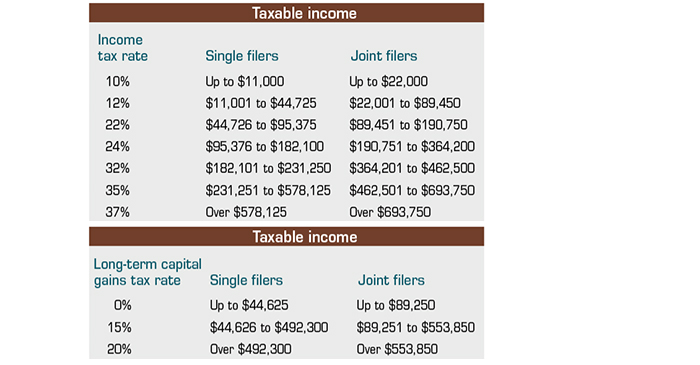

Capital gains and losses are classified as long term if the investment was held for more than one year, and short term if it was held for one year or less. Long-term gains are taxed at a rate of 0%, 15%, or 20% depending on your income. Short-term gains are taxed at your ordinary income tax rate, which may be much higher than your capital gains rate. High-income taxpayers (with modified adjusted gross income above $200,000 for single filers or $250,000 for joint filers) may also be subject to a 3.8% net investment income tax.

For tax purposes, capital losses are applied first to like capital gains and then to the other type of gains; for example, long-term losses are applied first to long-term gains and then to short-term gains. Up to $3,000 of any remaining losses can then be applied to your ordinary income for the current year ($1,500 if you are married filing separately). Finally, any remaining losses can be carried over to be applied to capital gains or ordinary income in future years. For most taxpayers, the biggest benefit comes when applying losses to short-term gains or ordinary income.

2023 Income and Capital Gains Tax Rates

Selling, buying, and washing

Some investors sell losing investments with the idea of harvesting the tax loss and then buying the same investment while its price remains low. To discourage this practice, the IRS has a wash-sale rule, which prohibits buying “substantially identical stock or securities” within 30 days prior to or after a sale. This also applies to securities purchased by your spouse or a company you own.

Under the right circumstances, harvesting a tax loss and then buying the same security at least 30 days later (i.e., after the wash-sale period expires) could potentially result in a lower tax liability when you sell that security later at a gain. This is most likely if you repurchase the security at a similar or lower price, and you are in a higher tax bracket at the time you take the loss than at the time you take the gain — for example, if you take the loss while working and sell when you are retired. Any year in which your taxable income falls within range for the 0% capital gains rate may be an opportune time to take gains, and any losses in that year would be applied to short-term gains or ordinary income.

Tax-loss harvesting is a complex strategy. It would be wise to consult your financial professional before taking action.

All investing involves risk, including the possible loss of principal. There is no guarantee that working with a financial professional will improve investment results, or that any investment strategy will be successful.